You’ve worked hard for your money. The last thing you want is to wake up one morning and find out you’ve lost a big chunk of it because the stock market went haywire. At the same time, leaving your cash in a regular savings account feels like watching it slowly shrink. With inflation still hovering around, money that’s not growing is actually losing value.Low Risk Investment Plans with High Returns in USA

So what do you do?

You look for the sweet spot. You look for low risk investment plans that can still give you solid, dependable returns. The kind of investments that let you sleep at night but also help you build wealth over time.

I get it. Finding those plans feels like searching for a unicorn. But here’s the good news: 2026 is actually a great year for conservative investors. Interest rates have settled into a “new normal,” bonds are attractive again, and there are plenty of options that balance safety with growth .

In this guide, I’m going to walk you through the best low risk investment plans available in the USA right now. We’ll look at Treasury bonds, high-yield savings accounts, real estate investment trusts, dividend stocks, and more. By the time you’re done reading, you’ll have a clear roadmap for your money.

Let’s dive in.How to open Brokerage Account.

What Does “Low Risk” Really Mean?

Before we start listing specific plans, we need to get on the same page about risk.Low Risk Investment Plans with High Returns in USA

Nothing in investing is 100% guaranteed. Even the safest options have some risk. When we talk about low risk investment plans, we mean investments that have:

- High principal stability: Your original money is very unlikely to disappear.

- Predictable income: You know roughly what you’ll earn.

- Government or institutional backing: There’s a strong entity standing behind the investment.

The trade-off? Lower risk usually means lower potential returns than you might get from stocks or crypto. But in 2026, with the Federal Reserve rates where they are, “lower risk” doesn’t mean “low return.” You can actually build meaningful wealth with safety .Low Risk Investment Plans with High Returns in USA

Why 2026 Is a Sweet Spot for Low Risk Investors

Here’s something you might not realize. The past few years have been rough for bonds and other conservative investments because interest rates kept rising. When rates go up, the value of existing bonds goes down.

But in 2026, the landscape has shifted.

The Federal Reserve has signaled that it’s done raising rates for now. Inflation is moderating. The yield curve is normalizing . For investors, this means:

- Bond prices are stabilizing: You’re not fighting against rate hikes anymore.

- Yields are attractive: You can lock in rates that actually beat inflation.

- Income is back: After years of near-zero returns, “boring” investments pay again.

According to Vanguard and Principal Asset Management, fixed income investments are entering 2026 on solid footing . That makes this the perfect time to explore low risk investment plans.

The Best Low Risk Investment Plans in the USA for 2026

Let’s get to the good stuff. Here are the top options for conservative investors this year.

1. High-Yield Savings Accounts and Money Market Funds

Sometimes the simplest option is the best. High-yield savings accounts and money market funds are about as safe as it gets. Your money is FDIC-insured (for bank accounts) or SIPC-protected (for money market funds), and you can access it anytime.Low Risk Investment Plans with High Returns in USA

Why they’re low risk:

- FDIC insurance covers up to $250,000 per depositor

- Principal is stable—it doesn’t go up and down

- Highly liquid (you can withdraw anytime)

What they pay in 2026:

With the Fed funds rate currently between 3.5% and 3.75%, high-yield savings accounts are offering around 3.5% to 4.25% . Money market funds are in a similar range.Low Risk Investment Plans with High Returns in USA

Best for:

- Emergency funds

- Short-term savings goals (under 3 years)

- Money you might need quickly

The catch: Rates can change. If the Fed cuts rates further, your interest payments will go down.

2. U.S. Treasury Securities

When people talk about the safest investments in the world, U.S. Treasuries top the list. They’re backed by the full faith and credit of the U.S. government. Default risk is basically zero.

Types of Treasuries:

- T-bills: Mature in a few days up to 52 weeks. You buy them at a discount and get full face value at maturity.

- T-notes: Mature in 2 to 10 years. They pay interest every six months.

- T-bonds: Mature in 20 or 30 years. Higher interest but more price fluctuation.

What they pay in 2026:

Short-term T-bills are yielding around 4% to 4.5%. Longer-term notes are in the 4.25% to 5% range .

Best for:

- Conservative investors who want government backing

- Building a ladder of maturities for steady income

- State tax advantages (Treasury interest is exempt from state and local taxes)

The catch: If you sell a Treasury before it matures, you could get less than you paid if interest rates have risen.

According to Vanguard’s 2026 outlook, bonds (including Treasuries) are positioned to provide income, endurance, and diversification in a balanced portfolio .

3. Investment-Grade Corporate Bonds and ETFs

Companies with strong balance sheets borrow money by issuing bonds. These bonds pay higher interest than Treasuries because there’s slightly more risk. But “investment-grade” means the company is financially solid.Low Risk Investment Plans with High Returns in USA

Why they’re relatively low risk:

- Companies rated BBB or higher have low default risk

- You get regular interest payments

- Bondholders get paid before stockholders if the company runs into trouble

What they pay in 2026:

Investment-grade corporate bonds are currently yielding between 4.25% and 5.25% . You can buy individual bonds or bond ETFs for instant diversification.Low Risk Investment Plans with High Returns in USA

Best for:

- Income-focused investors

- Diversifying away from government bonds

- Investors who want higher yields than Treasuries without huge risk

The catch: Corporate bonds can lose value if the company’s financial health declines or if interest rates rise.

Money Talks News notes that bond ETFs are emerging as a premier tool for protecting gains and capturing steady yields in the shifting 2026 economy .

4. Municipal Bonds

If you’re in a higher tax bracket, municipal bonds (“munis”) deserve a close look. These are bonds issued by states, cities, and local governments. The interest is generally exempt from federal income tax, and often from state tax if you live in the issuing state.Low Risk Investment Plans with High Returns in USA

Why they’re low risk:

- Backed by local governments with taxing authority

- Default rates are historically very low

- Tax advantages boost your after-tax return

What they pay in 2026:

Taxable-equivalent yields can be very attractive for high-income investors. Principal Asset Management notes that munis benefit from steep curves and favorable taxable-equivalent yields .

Best for:

- Investors in high tax brackets

- Those seeking tax-free income

- Conservative portfolios focused on income

The catch: You need to understand the credit quality of the issuing government. General obligation bonds are safer than revenue bonds.Low Risk Investment Plans with High Returns in USA

5. Certificates of Deposit (CDs)

CDs are time deposits with banks. You agree to leave your money for a set period—from a few months to several years—and the bank pays you a fixed interest rate.

Why they’re low risk:

- FDIC insured up to $250,000

- Fixed, guaranteed interest rate

- Principal is safe if you hold to maturity

What they pay in 2026:

CD rates vary by term and bank, but you can find 1-year CDs around 4% to 4.5% and 5-year CDs around 4.25% to 4.75%.

Best for:

- Conservative savers

- Building a CD ladder for regular maturities

- Money you won’t need for a specific period

The catch: Early withdrawal penalties can eat into your interest if you need the money before maturity.Low Risk Investment Plans with High Returns in USA

6. Real Estate Investment Trusts (REITs)

Now we’re getting into options that offer higher potential returns but come with a bit more volatility. Real Estate Investment Trusts own and operate income-producing real estate. They’re required to pay out most of their income as dividends.Low Risk Investment Plans with High Returns in USA

Why they’re attractive:

- High dividend yields (often 4% to 6% or more)

- Professional management of real estate assets

- Liquidity (you can buy and sell REITs on stock exchanges)

The low risk angle:

While REITs can be volatile in the short term, high-quality REITs with strong balance sheets and diversified portfolios have proven resilient over time. According to The Motley Fool, the Vanguard Real Estate Index Fund (VNQ) pays an above-average dividend yield (around 4%) and could be a low-risk but high-potential investment opportunity .Low Risk Investment Plans with High Returns in USA

Best for:

- Income investors who want exposure to real estate

- Diversification away from stocks and bonds

- Long-term holders who can ride out short-term price swings

The catch: REIT prices can drop during economic downturns or when interest rates rise. Not all REITs are created equal—focus on quality.Low Risk Investment Plans with High Returns in USA

7. Dividend Aristocrats

These are companies in the S&P 500 that have increased their dividends for at least 25 consecutive years. They tend to be stable, profitable businesses with durable competitive advantages.

Examples include:

- Realty Income: A REIT with 30 consecutive years of dividend increases and a forward yield near 5.8%

- Verizon: A telecom giant with 19 consecutive years of dividend increases and a yield around 6.8%

- Enbridge: An energy infrastructure company with 31 consecutive years of dividend increases and a yield over 5.8%

Why they’re relatively low risk:

- Long track records of surviving tough times

- Essential products and services (people need telecom, energy, etc.)

- Consistent cash flow supports dividend payments

Best for:

- Dividend-focused investors

- Long-term wealth building

- Those who want growing income over time

The catch: Even stable stocks can drop in price. Dividends can be cut in extreme circumstances, though these companies have strong histories.Low Risk Investment Plans with High Returns in USA

8. Infrastructure Investments

Infrastructure is emerging as one of the most compelling low-risk opportunities for 2026. According to Forbes, infrastructure investments offer durable income paired with long-term growth .

Why infrastructure is attractive:

- Essential services (energy, transportation, data centers)

- Often supported by government policy and public-private partnerships

- Lower volatility than traditional private equity

- Inflation protection built into many contracts

J.P. Morgan positions infrastructure as a beneficiary of powerful forces including grid modernization, the energy transition, and data center growth driven by AI .

Best for:

- Investors seeking steady, inflation-protected income

- Those who want exposure to AI without tech stock volatility

- Long-term portfolios focused on essential assets

The catch: Some infrastructure funds have high minimums and long lock-up periods. Look for hybrid options or ETFs for easier access.Low Risk Investment Plans with High Returns in USA

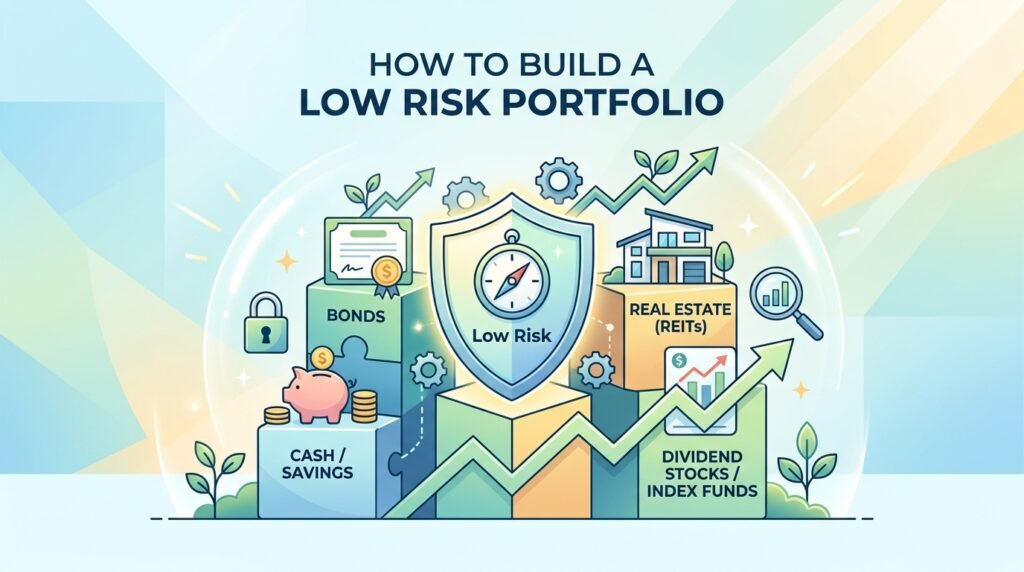

How to Build a Low Risk Portfolio

Now that you know the options, how do you put them together? Here’s a simple framework.

The Conservative Income Portfolio

Goal: Steady income with minimal volatility

- 30% Short-term Treasuries (T-bills, 1-3 year notes)

- 30% Investment-grade corporate bond ETFs

- 20% High-yield savings / Money market

- 10% Municipal bonds (if tax-advantaged)

- 10% Dividend Aristocrats (for growth)

The Balanced Conservative Portfolio

Goal: Income plus some growth potential

- 25% Intermediate-term bond ETFs

- 20% Dividend Aristocrats / REITs

- 20% Treasuries (mix of short and intermediate)

- 15% CDs / High-yield savings

- 10% Infrastructure investments

- 10% International bonds (for diversification)

The Retirement Income Portfolio

Goal: Sustainable withdrawals for retirees

- 30% Bond ladder (Treasuries and corporate)

- 25% Dividend growth stocks

- 20% REITs and infrastructure

- 15% Annuities (if appropriate)

- 10% Cash reserves

What to Avoid in 2026

Even within low risk investing, there are traps. Here’s what to watch out for.

Don’t Chase Yield Unwisely

High yield usually means high risk. Be skeptical of any investment promising 8% or more with “no risk.” That combination doesn’t exist in the real world.

Avoid Long-Term Bonds If You Might Need the Money

Long-term bonds (20-30 years) can drop significantly in price if rates rise. If you might need to sell before maturity, stick with shorter durations.

Be Careful with Junk Bonds

High-yield (“junk”) bonds offer tempting yields, but default risk rises during economic slowdowns. Stick with investment-grade unless you’re willing to take on more risk .Low Risk Investment Plans with High Returns in USA

Don’t Overlook Fees

Low risk doesn’t mean low cost. High fees can eat up your returns. Look for low-cost ETFs and mutual funds with expense ratios under 0.1% for core holdings .

Frequently Asked Questions

Q: What are the safest low risk investment plans in the USA?

A: The safest options are U.S. Treasury securities, FDIC-insured high-yield savings accounts, and Certificates of Deposit (CDs). These have government backing or insurance, making principal loss extremely unlikely .

Q: Can low risk investments really give high returns?

A: “High returns” is relative. In 2026, you can earn 4% to 6% with well-chosen low risk investment plans, which beats inflation and far exceeds savings account rates from a few years ago. For true safety, temper your expectations .

Q: What’s the difference between a bond and a bond ETF?

A: An individual bond has a fixed maturity date and fixed interest payments. A bond ETF holds many bonds and trades like a stock. ETFs offer instant diversification but don’t mature, so their price fluctuates with the market .

Q: Are REITs considered low risk?

A: REITs are not as safe as bonds or savings accounts, but high-quality REITs like Realty Income have long histories of stable dividends and can be part of a diversified low-risk portfolio .

Q: How much should I keep in cash versus investments?

A: Most experts recommend keeping 3-6 months of expenses in cash (high-yield savings or money market). The rest can be invested in low risk investment plans that offer higher returns.

Q: What are the best low risk investment plans for retirees?

A: Retirees often favor a mix of: Treasury bonds (safety), municipal bonds (tax-free income), high-quality dividend stocks (growth), and CDs (stable principal). A bond ladder can provide predictable income .

Q: How do I start investing with low risk?

A: Start with a high-yield savings account to build your emergency fund. Then consider opening a brokerage account and buying short-term Treasury ETFs or a diversified bond fund. Work with a fee-only advisor if you have over $100,000 .

Safety and Growth Can Coexist

You don’t have to choose between sleeping well at night and building wealth. In 2026, thanks to a more stable interest rate environment and a wide range of quality investments, you can have both.

The key is knowing where to look. U.S. Treasuries, high-yield savings, CDs, investment-grade bonds, municipal bonds, quality REITs, dividend aristocrats, and infrastructure investments all offer attractive combinations of safety and return.

Start by assessing your own goals and time horizon. How much income do you need? When will you need your money? How much volatility can you stomach?

Then build a diversified mix of low risk investment plans that fit your answers. Stick to quality. Keep fees low. And remember: slow and steady really can win the race.

Your future self—the one with a growing nest egg and zero sleepless nights—will thank you.

Here’s to smart, safe investing in 2026.